Over the last six months, Littelfuse’s shares have sunk to $231.01, producing a disappointing 13% loss - a stark contrast to the S&P 500’s 4.2% gain. This might have investors contemplating their next move.

Is now the time to buy Littelfuse, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Even though the stock has become cheaper, we don't have much confidence in Littelfuse. Here are three reasons why you should be careful with LFUS and a stock we'd rather own.

Why Is Littelfuse Not Exciting?

The developer of the first blade-type automotive fuse, Littelfuse (NASDAQ:LFUS) provides electrical protection and control components for the automotive, industrial, electronics, and telecommunications industries.

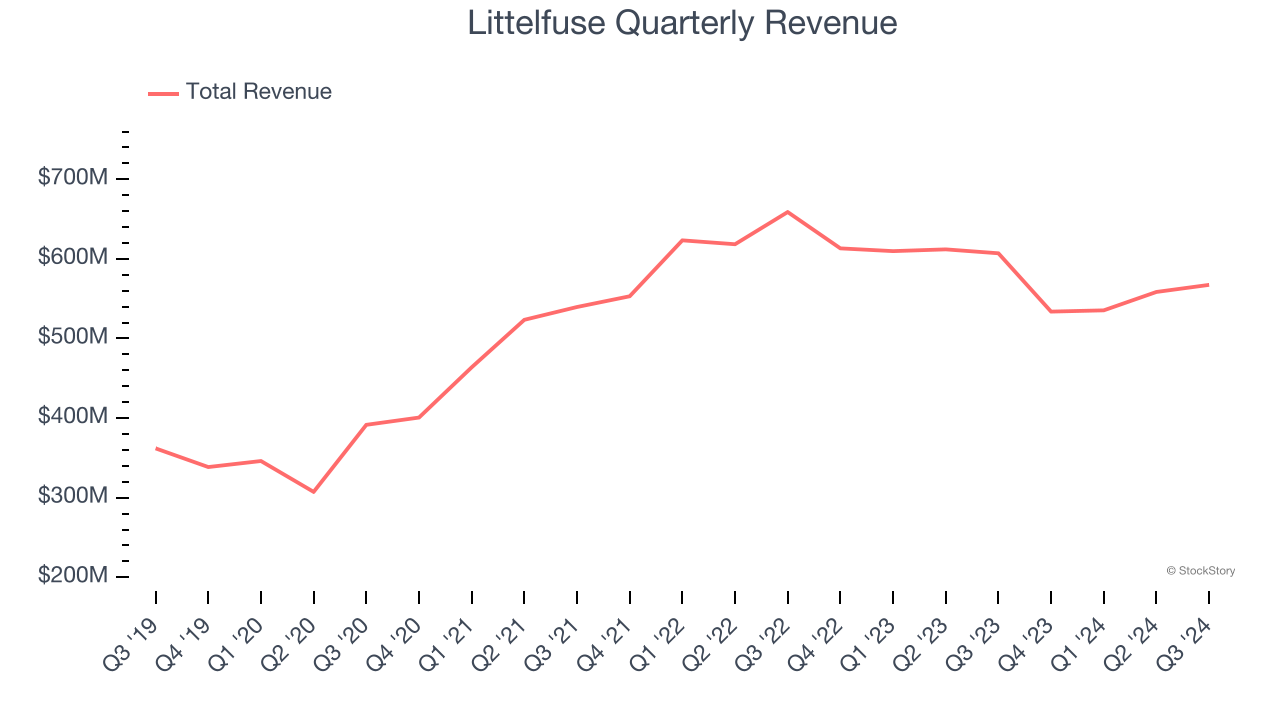

1. Long-Term Revenue Growth Disappoints

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Regrettably, Littelfuse’s sales grew at a mediocre 7% compounded annual growth rate over the last five years. This fell short of our benchmark for the industrials sector.

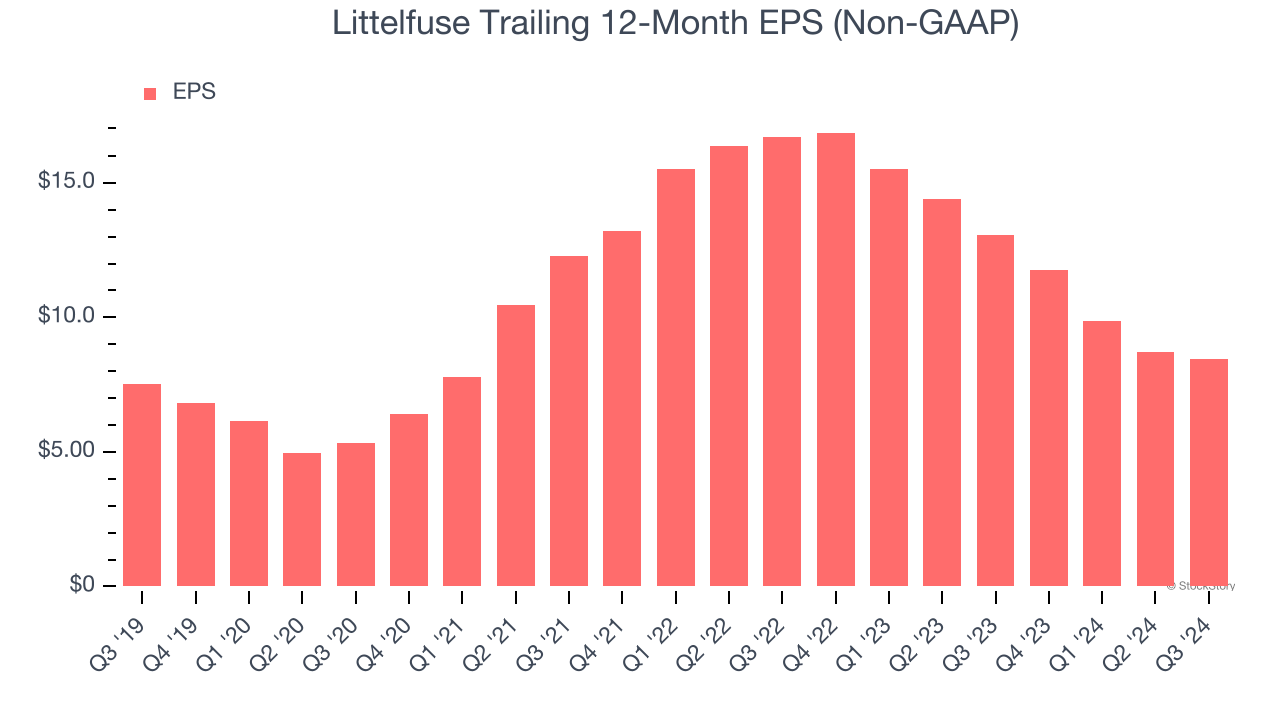

2. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Littelfuse’s EPS grew at a weak 2.4% compounded annual growth rate over the last five years, lower than its 7% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

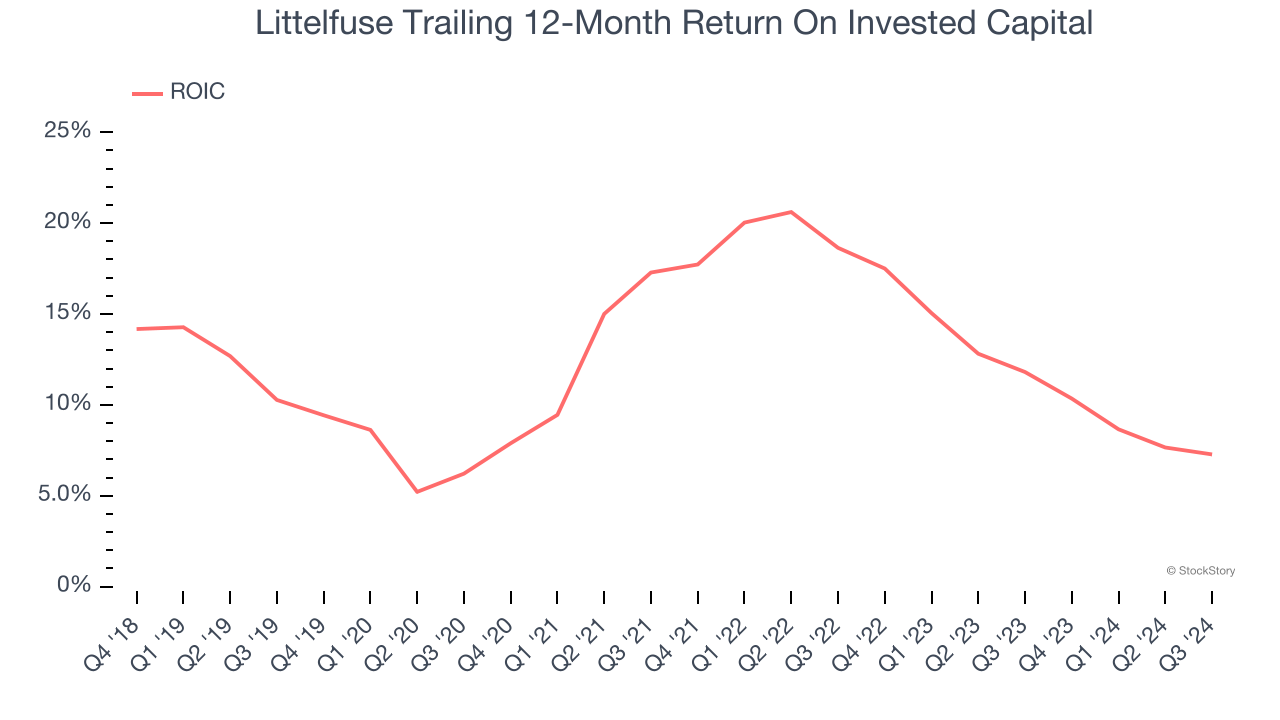

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We typically prefer to invest in companies with high returns because it means they have viable business models, but the trend in a company’s ROIC is often what surprises the market and moves the stock price. Unfortunately, Littelfuse’s ROIC averaged 2.2 percentage point decreases over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

Littelfuse isn’t a terrible business, but it doesn’t pass our bar. After the recent drawdown, the stock trades at 21.9× forward price-to-earnings (or $231.01 per share). This multiple tells us a lot of good news is priced in - we think there are better investment opportunities out there. We’d recommend looking at The Trade Desk, the nucleus of digital advertising.

Stocks We Would Buy Instead of Littelfuse

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.