Let’s dig into the relative performance of GitLab (NASDAQ:GTLB) and its peers as we unravel the now-completed Q3 software development earnings season.

As legendary VC investor Marc Andreessen says, "Software is eating the world", and it touches virtually every industry. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming.

The 11 software development stocks we track reported a strong Q3. As a group, revenues beat analysts’ consensus estimates by 3.3% while next quarter’s revenue guidance was 0.7% above.

In light of this news, share prices of the companies have held steady as they are up 2.2% on average since the latest earnings results.

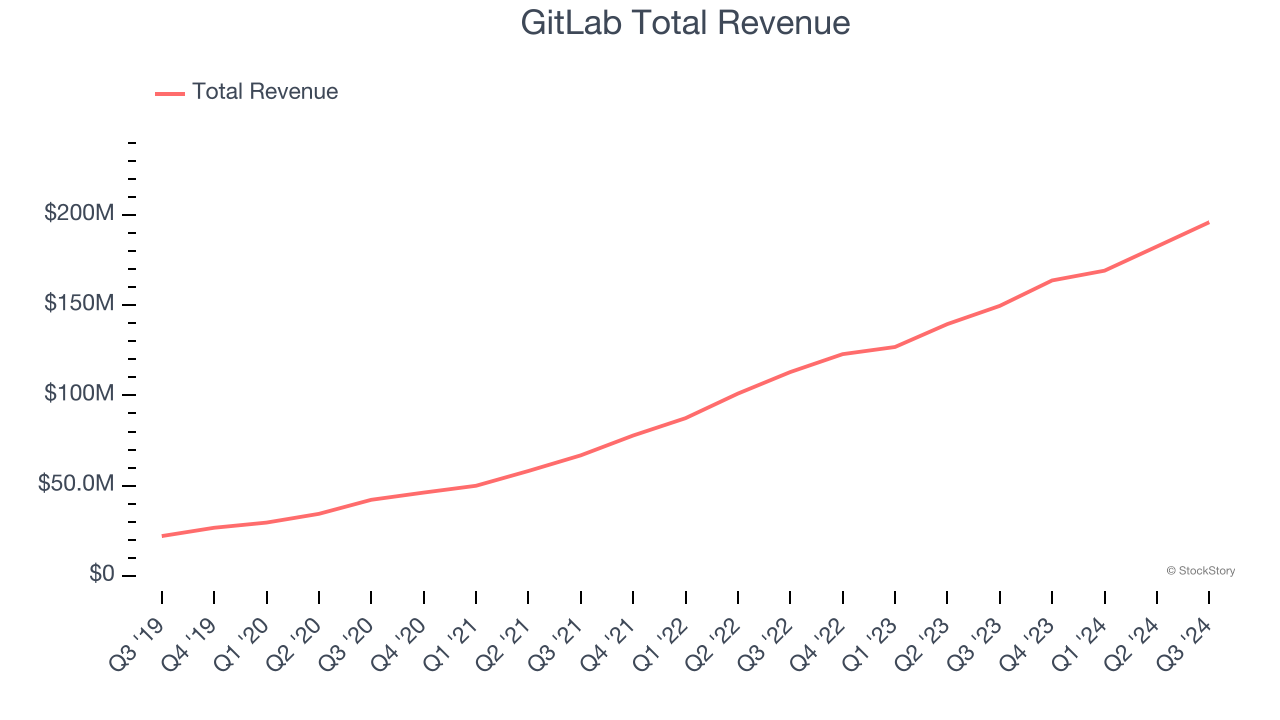

GitLab (NASDAQ:GTLB)

Founded as an open-source project in 2011, GitLab (NASDAQ:GTLB) is a leading software development tools platform.

GitLab reported revenues of $196 million, up 31% year on year. This print exceeded analysts’ expectations by 4.1%. Overall, it was a strong quarter for the company with EPS guidance for next quarter exceeding analysts’ expectations and a solid beat of analysts’ EBITDA estimates.

“GitLab’s growth at scale is a testament to the demand for a platform approach to software development,” said Sid Sijbrandij, co-founder and executive chair of the board of directors,

GitLab scored the fastest revenue growth of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 12.1% since reporting and currently trades at $58.10.

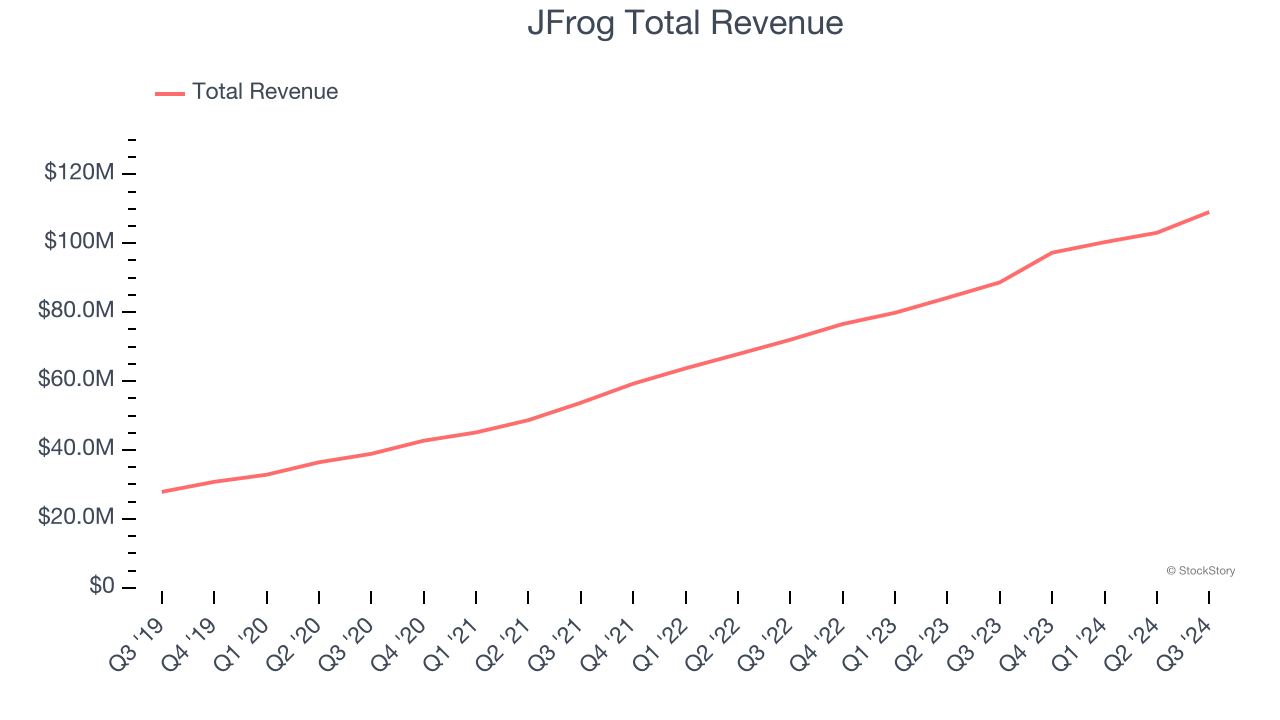

Best Q3: JFrog (NASDAQ:FROG)

Named after the founders' affinity for frogs, JFrog (NASDAQ:FROG) provides a software-as-a-service platform that makes developing and releasing software easier and faster, especially for large teams.

JFrog reported revenues of $109.1 million, up 23% year on year, outperforming analysts’ expectations by 3.3%. The business had a very strong quarter with an impressive beat of analysts’ billings estimates and accelerating growth in large customers.

Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 6.1% since reporting. It currently trades at $30.89.

Is now the time to buy JFrog? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Akamai (NASDAQ:AKAM)

Founded in 1999 by two engineers from MIT, Akamai (NASDAQ:AKAM) provides software for organizations to efficiently deliver web content to their customers.

Akamai reported revenues of $1.00 billion, up 4.1% year on year, exceeding analysts’ expectations by 0.5%. Still, it was a slower quarter as it posted revenue guidance for the next quarter below analysts’ expectations.

Akamai delivered the weakest performance against analyst estimates, slowest revenue growth, and weakest full-year guidance update in the group. As expected, the stock is down 14% since the results and currently trades at $89.75.

Read our full analysis of Akamai’s results here.

F5 (NASDAQ:FFIV)

Initially started as a hardware appliances company in the late 1990s, F5 (NASDAQ:FFIV) makes software that helps large enterprises ensure their web applications are always available by distributing network traffic and protecting them from cyberattacks.

F5 reported revenues of $746.7 million, up 5.6% year on year. This number topped analysts’ expectations by 2.2%. Overall, it was a strong quarter as it also put up a solid beat of analysts’ billings estimates and revenue guidance for next quarter slightly topping analysts’ expectations.

The stock is up 15.6% since reporting and currently trades at $252.63.

Read our full, actionable report on F5 here, it’s free.

Cloudflare (NYSE:NET)

Founded by two grad students of Harvard Business School, Cloudflare (NYSE:NET) is a software-as-a-service platform that helps improve the security, reliability, and loading times of internet applications.

Cloudflare reported revenues of $430.1 million, up 28.2% year on year. This print surpassed analysts’ expectations by 1.4%. It was a strong quarter as it also recorded an impressive beat of analysts’ EBITDA estimates and full-year EPS guidance exceeding analysts’ expectations.

The stock is up 16.6% since reporting and currently trades at $111.62.

Read our full, actionable report on Cloudflare here, it’s free.

Market Update

Thanks to the Fed's series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market has thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% each in November and December), and a notable surge followed Donald Trump's presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by the pace and magnitude of future rate cuts as well as potential changes in trade policy and corporate taxes once the Trump administration takes over. The path forward is marked by uncertainty.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.