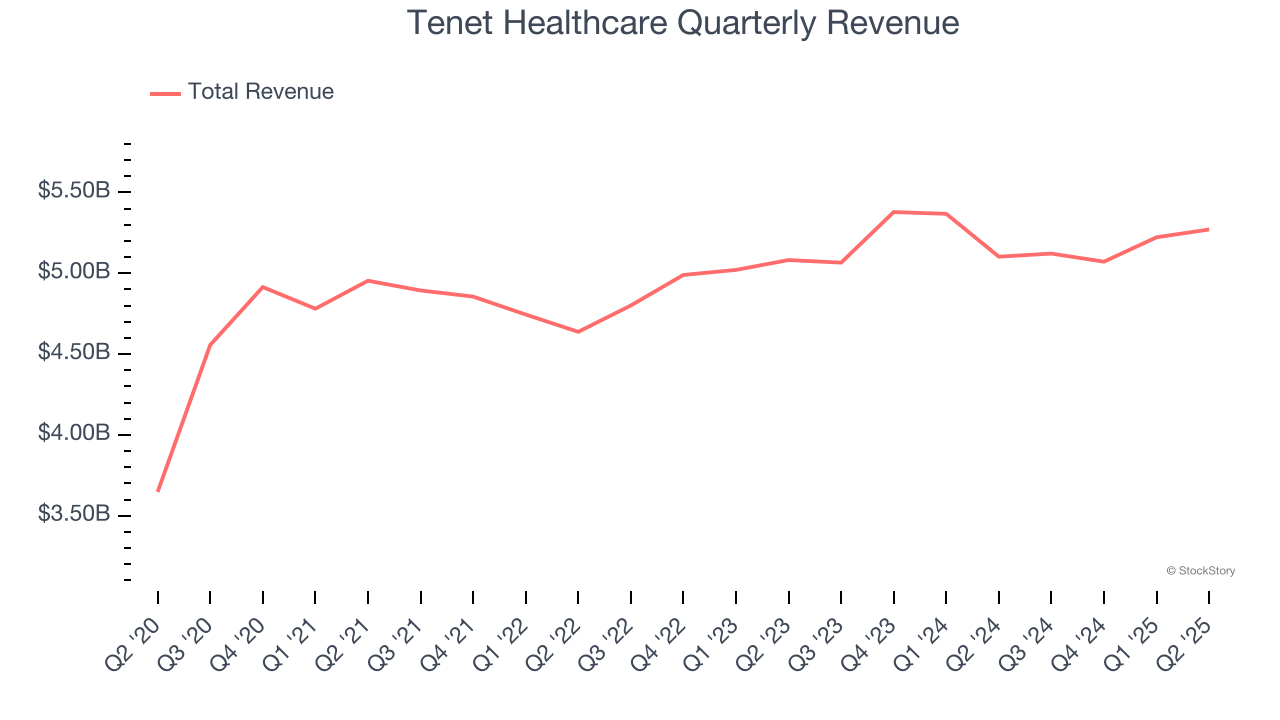

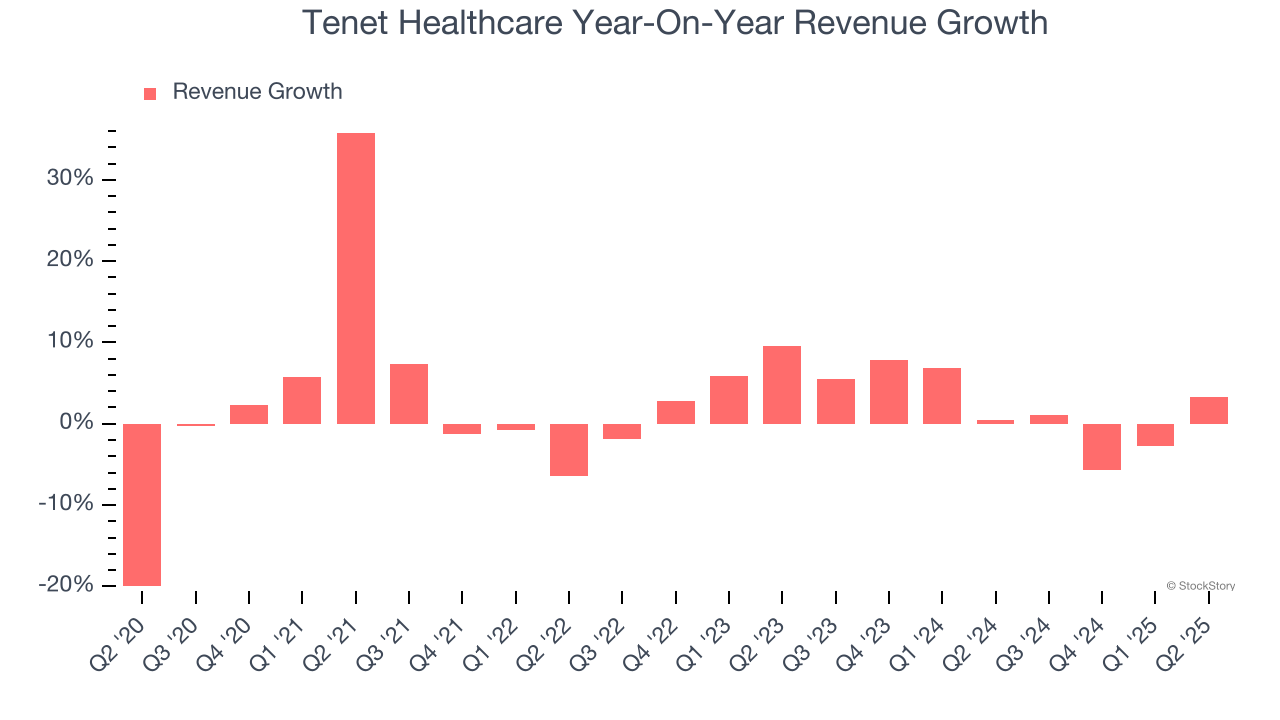

Hospital operator Tenet Healthcare (NYSE:THC) reported revenue ahead of Wall Street’s expectations in Q2 CY2025, with sales up 3.3% year on year to $5.27 billion. The company’s full-year revenue guidance of $21.1 billion at the midpoint came in 0.9% above analysts’ estimates. Its non-GAAP profit of $4.02 per share was 40.1% above analysts’ consensus estimates.

Is now the time to buy Tenet Healthcare? Find out by accessing our full research report, it’s free.

Tenet Healthcare (THC) Q2 CY2025 Highlights:

- Revenue: $5.27 billion vs analyst estimates of $5.15 billion (3.3% year-on-year growth, 2.3% beat)

- Adjusted EPS: $4.02 vs analyst estimates of $2.87 (40.1% beat)

- Adjusted EBITDA: $1.12 billion vs analyst estimates of $991.9 million (21.3% margin, 13% beat)

- The company lifted its revenue guidance for the full year to $21.1 billion at the midpoint from $20.8 billion, a 1.4% increase

- Management raised its full-year Adjusted EPS guidance to $15.88 at the midpoint, a 26.5% increase

- EBITDA guidance for the full year is $4.47 billion at the midpoint, above analyst estimates of $4.16 billion

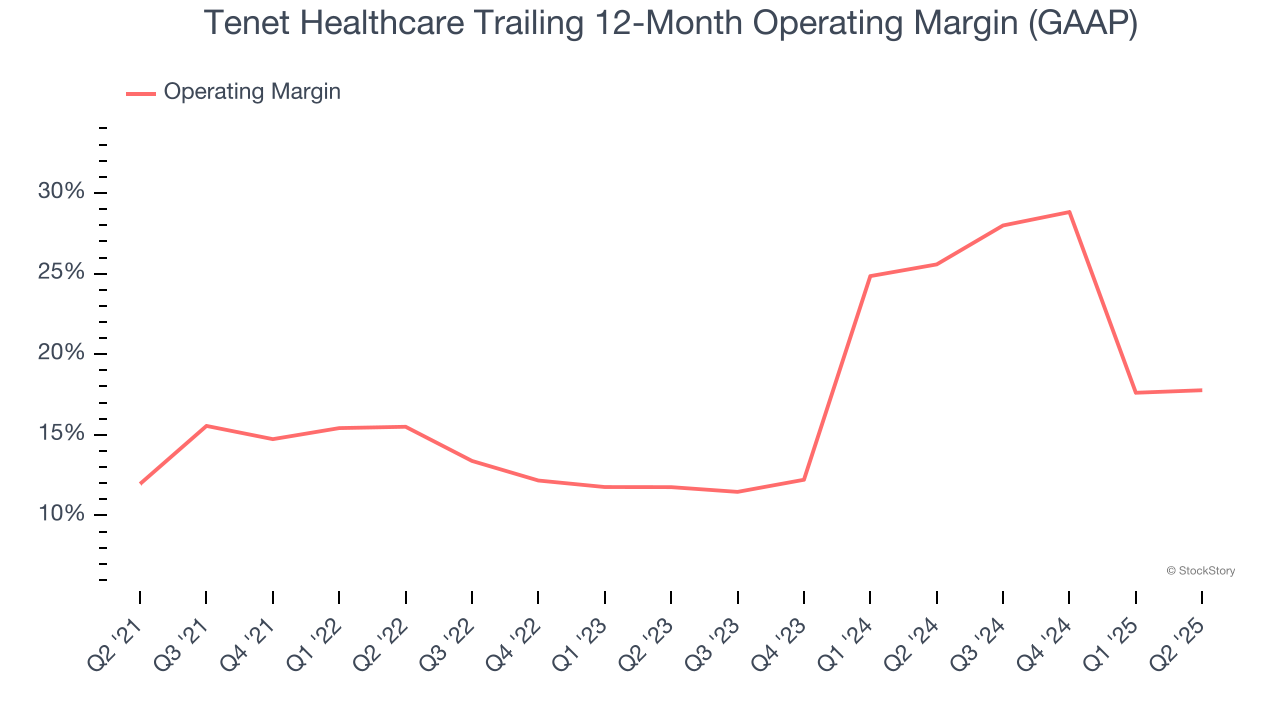

- Operating Margin: 15.6%, in line with the same quarter last year

- Free Cash Flow Margin: 14.1%, up from 11.8% in the same quarter last year

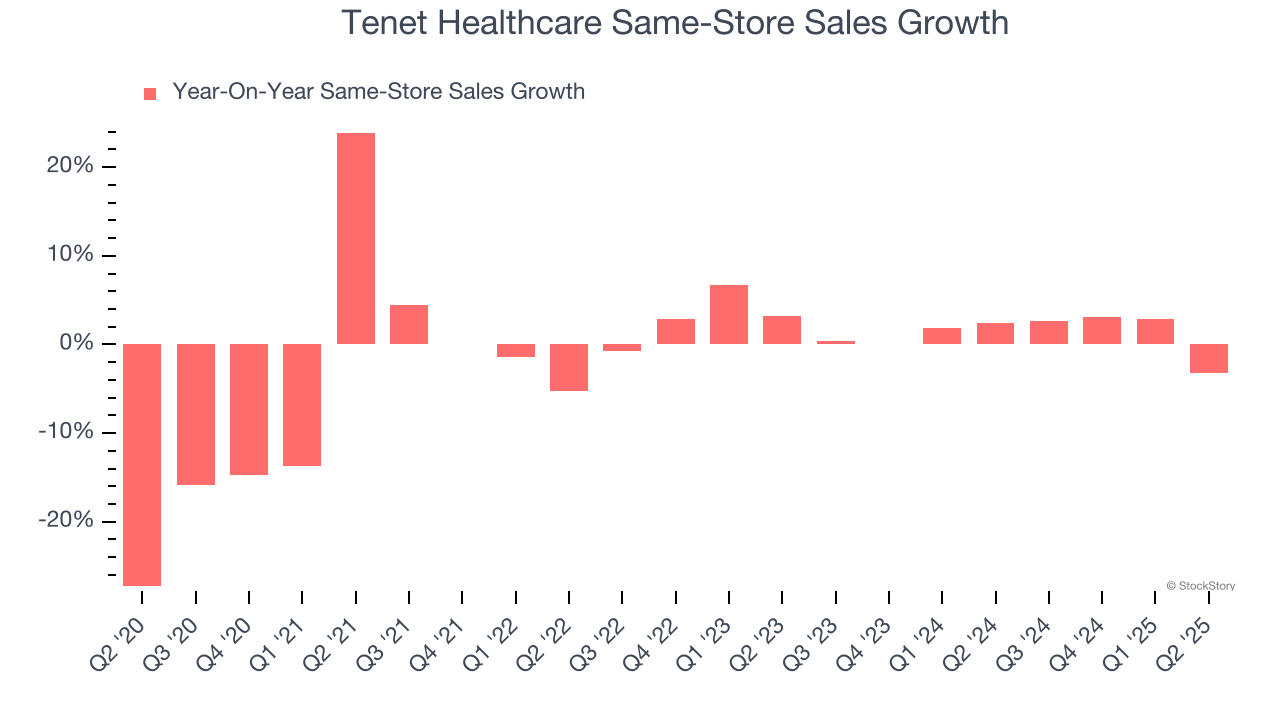

- Same-Store Sales fell 3.2% year on year (2.4% in the same quarter last year)

- Market Capitalization: $16.22 billion

"Our strong second quarter results extend our track record of attractive same store revenue growth, operational performance driven by fundamentals, and robust free cash flow generation," said Saum Sutaria, M.D., Chairman and Chief Executive Officer of Tenet.

Company Overview

With a network spanning nine states and serving primarily urban and suburban communities, Tenet Healthcare (NYSE:THC) operates a nationwide network of hospitals, ambulatory surgery centers, and outpatient facilities providing acute care and specialty healthcare services.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Tenet Healthcare’s sales grew at a tepid 3.4% compounded annual growth rate over the last five years. This wasn’t a great result compared to the rest of the healthcare sector, but there are still things to like about Tenet Healthcare.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Tenet Healthcare’s recent performance shows its demand has slowed as its annualized revenue growth of 2% over the last two years was below its five-year trend.

We can better understand the company’s revenue dynamics by analyzing its same-store sales, which show how much revenue its established locations generate. Over the last two years, Tenet Healthcare’s same-store sales averaged 1.3% year-on-year growth. This number doesn’t surprise us as it’s in line with its revenue growth.

This quarter, Tenet Healthcare reported modest year-on-year revenue growth of 3.3% but beat Wall Street’s estimates by 2.3%.

Looking ahead, sell-side analysts expect revenue to grow 3.3% over the next 12 months, similar to its two-year rate. While this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average. At least the company is tracking well in other measures of financial health.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Tenet Healthcare has managed its cost base well over the last five years. It demonstrated solid profitability for a healthcare business, producing an average operating margin of 16.7%.

Looking at the trend in its profitability, Tenet Healthcare’s operating margin rose by 5.8 percentage points over the last five years, as its sales growth gave it operating leverage. The company’s two-year trajectory shows its performance was mostly driven by its recent improvements.

In Q2, Tenet Healthcare generated an operating margin profit margin of 15.6%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

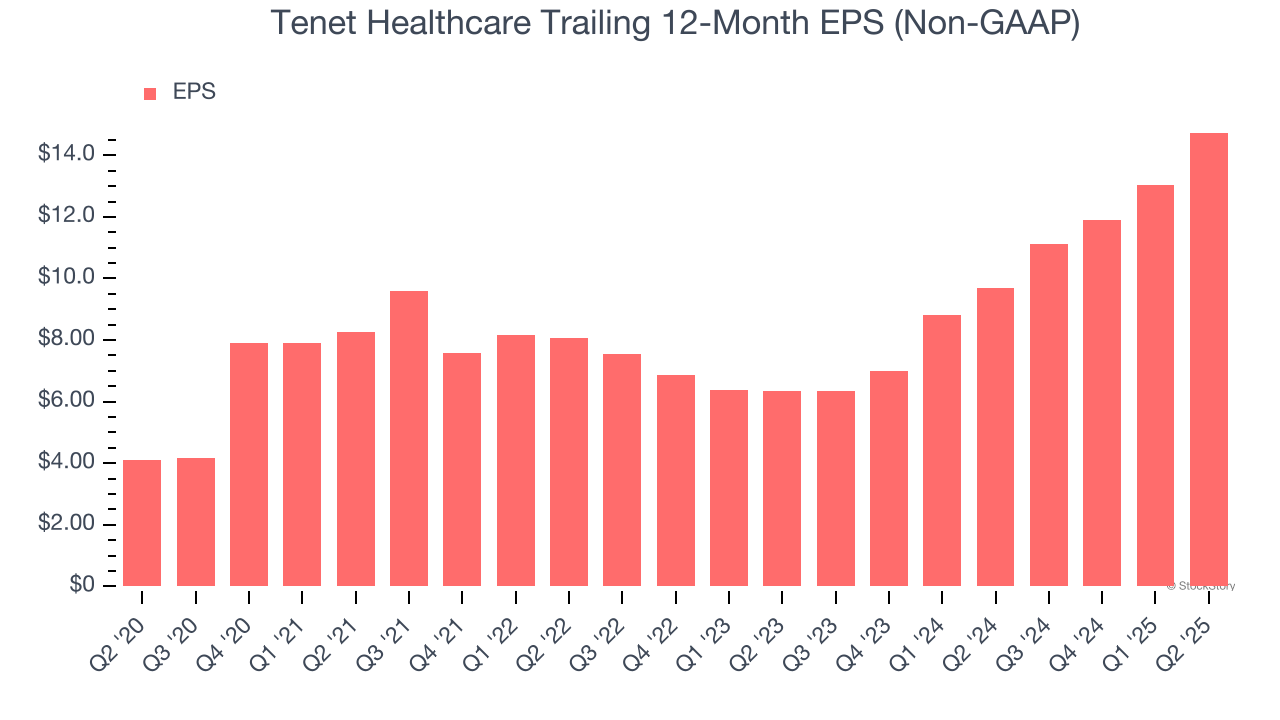

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Tenet Healthcare’s EPS grew at an astounding 29.1% compounded annual growth rate over the last five years, higher than its 3.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

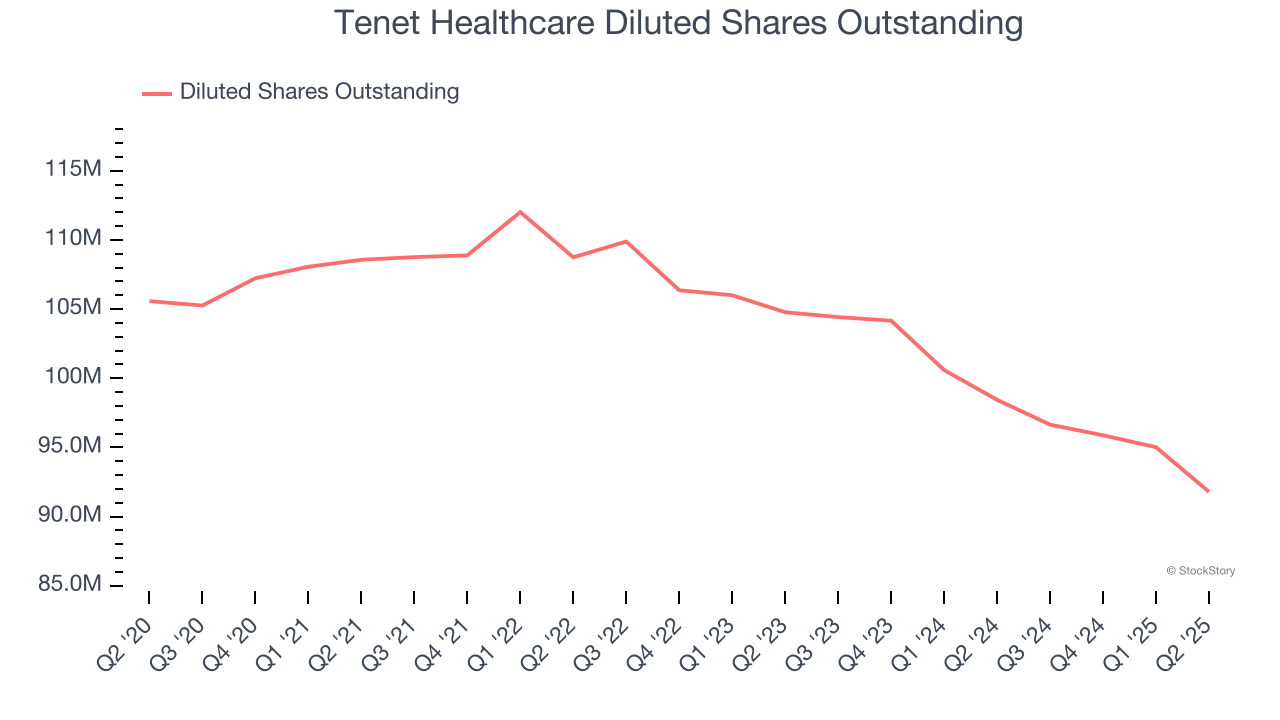

Diving into the nuances of Tenet Healthcare’s earnings can give us a better understanding of its performance. As we mentioned earlier, Tenet Healthcare’s operating margin was flat this quarter but expanded by 5.8 percentage points over the last five years. On top of that, its share count shrank by 13.1%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q2, Tenet Healthcare reported EPS at $4.02, up from $2.31 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Tenet Healthcare’s full-year EPS of $14.74 to shrink by 11.8%.

Key Takeaways from Tenet Healthcare’s Q2 Results

We were impressed by how significantly Tenet Healthcare blew past analysts’ EPS expectations this quarter. We were also excited its full-year EPS guidance outperformed Wall Street’s estimates by a wide margin. On the other hand, its same-store sales missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 1.8% to $178 immediately after reporting.

Sure, Tenet Healthcare had a solid quarter, but if we look at the bigger picture, is this stock a buy? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.