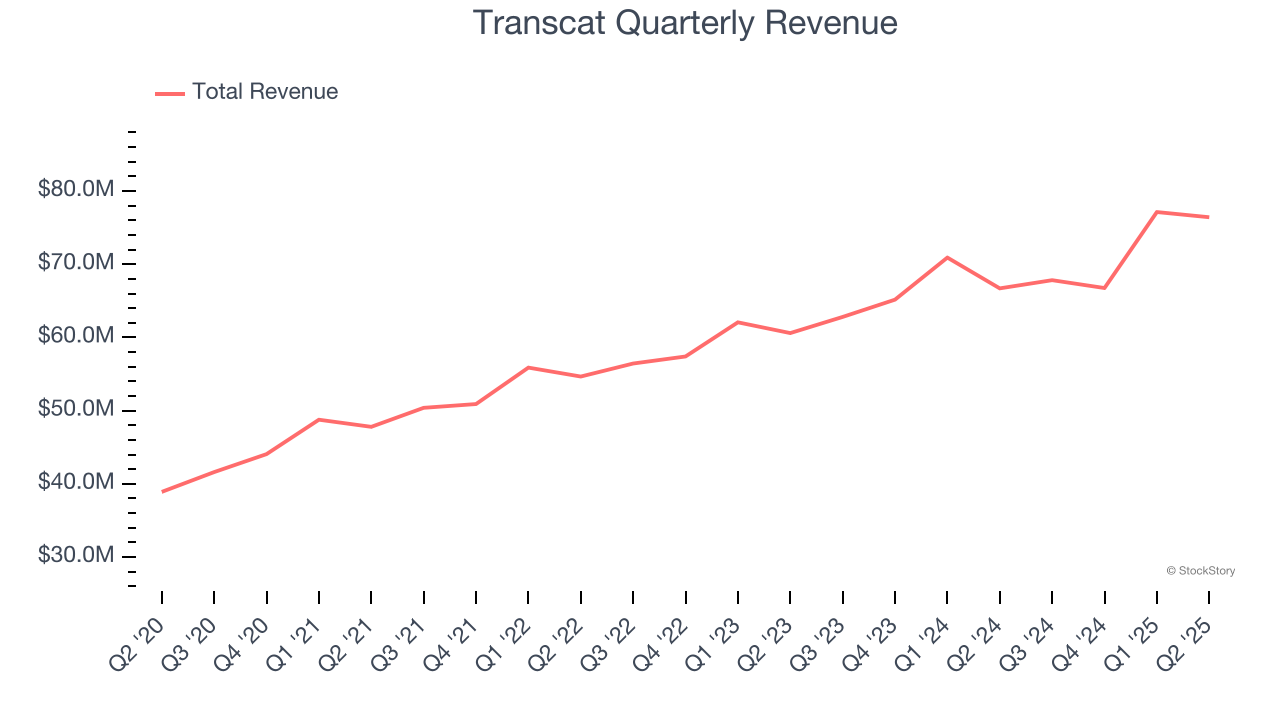

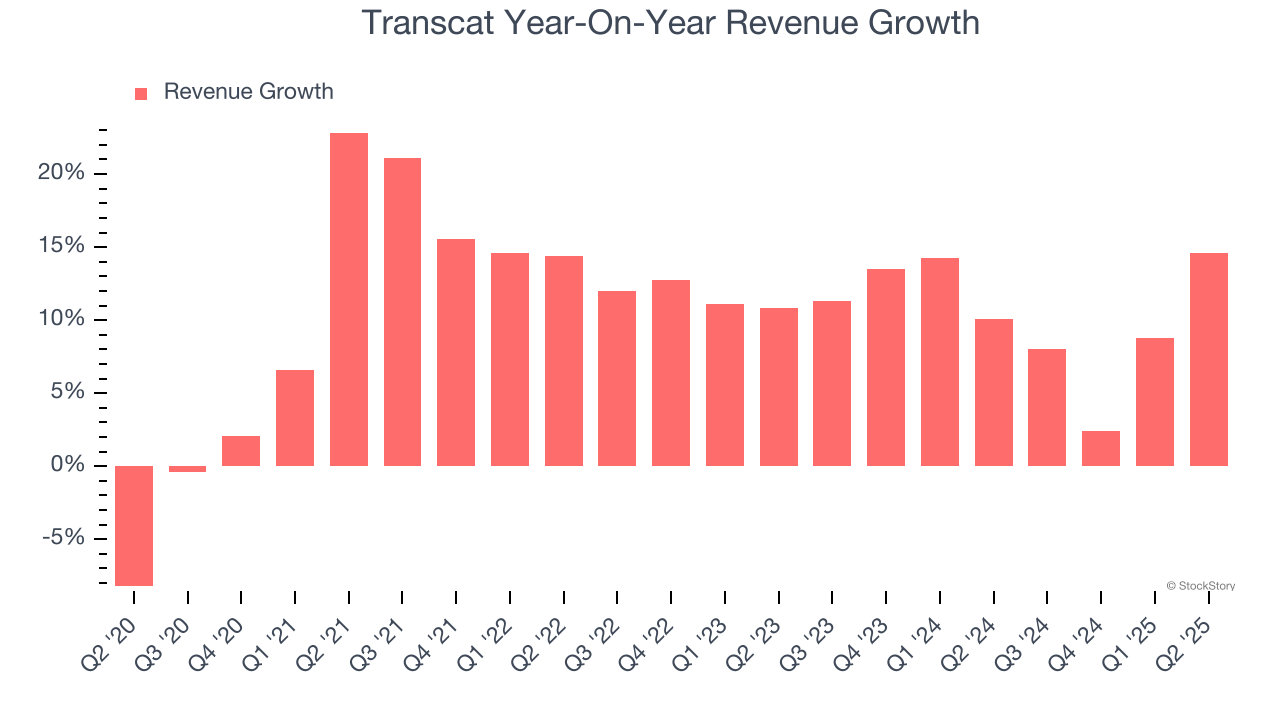

Measurement equipment distributor Transcat (NASDAQ:TRNS) reported Q2 CY2025 results topping the market’s revenue expectations, with sales up 14.6% year on year to $76.42 million. Its non-GAAP profit of $0.59 per share was 49% above analysts’ consensus estimates.

Is now the time to buy Transcat? Find out by accessing our full research report, it’s free.

Transcat (TRNS) Q2 CY2025 Highlights:

- Revenue: $76.42 million vs analyst estimates of $72.28 million (14.6% year-on-year growth, 5.7% beat)

- Adjusted EPS: $0.59 vs analyst estimates of $0.40 (49% beat)

- Adjusted EBITDA: $11.77 million vs analyst estimates of $9.51 million (15.4% margin, 23.8% beat)

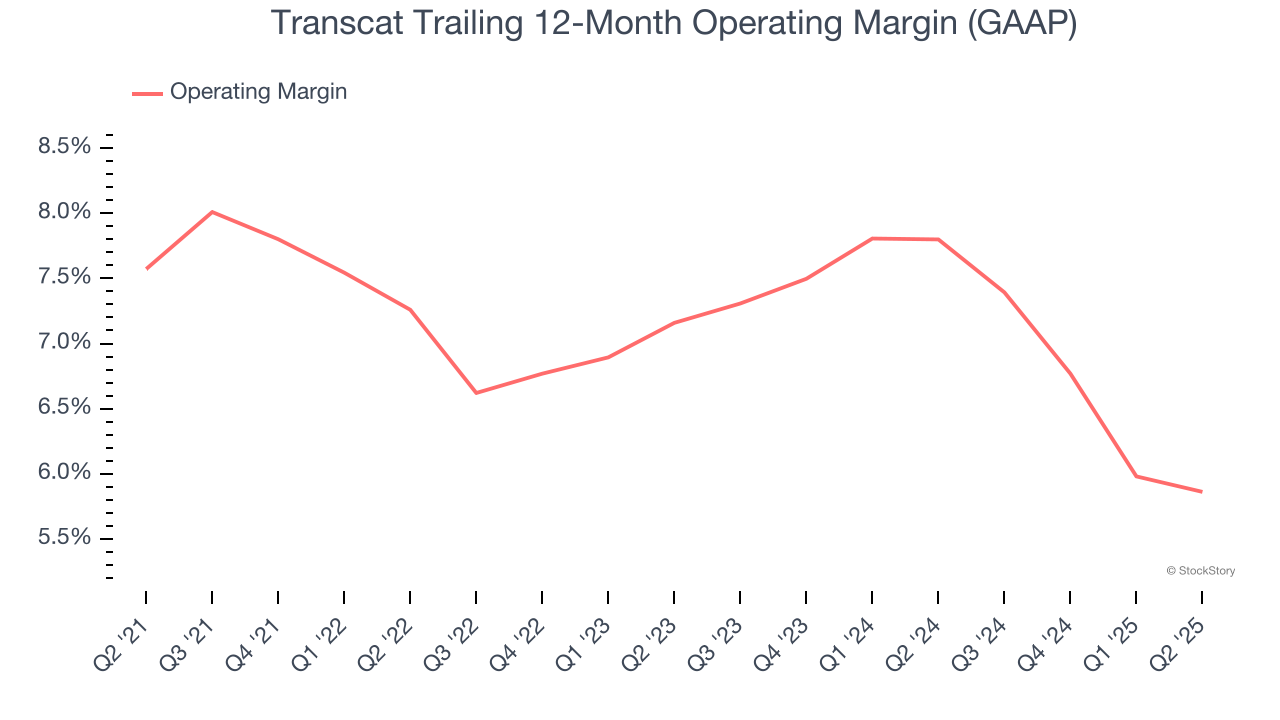

- Operating Margin: 7%, in line with the same quarter last year

- Free Cash Flow was -$975,000, down from $5.25 million in the same quarter last year

- Market Capitalization: $704.9 million

"The Transcat team delivered solid revenue and adjusted EBITDA performance in the fiscal first quarter highlighted by double-digit service revenue growth and better-than-expected demand in our distribution segment,” commented Lee D. Rudow, President and CEO.

Company Overview

Serving the pharmaceutical, industrial manufacturing, energy, and chemical process industries, Transcat (NASDAQ:TRNS) provides measurement instruments and supplies.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Transcat grew its sales at an impressive 11.2% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Transcat’s annualized revenue growth of 10.4% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

This quarter, Transcat reported year-on-year revenue growth of 14.6%, and its $76.42 million of revenue exceeded Wall Street’s estimates by 5.7%.

Looking ahead, sell-side analysts expect revenue to grow 8.8% over the next 12 months, a slight deceleration versus the last two years. Despite the slowdown, this projection is above average for the sector and suggests the market is baking in some success for its newer products and services.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Transcat was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.1% was weak for an industrials business.

Looking at the trend in its profitability, Transcat’s operating margin decreased by 1.7 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Transcat’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q2, Transcat generated an operating margin profit margin of 7%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

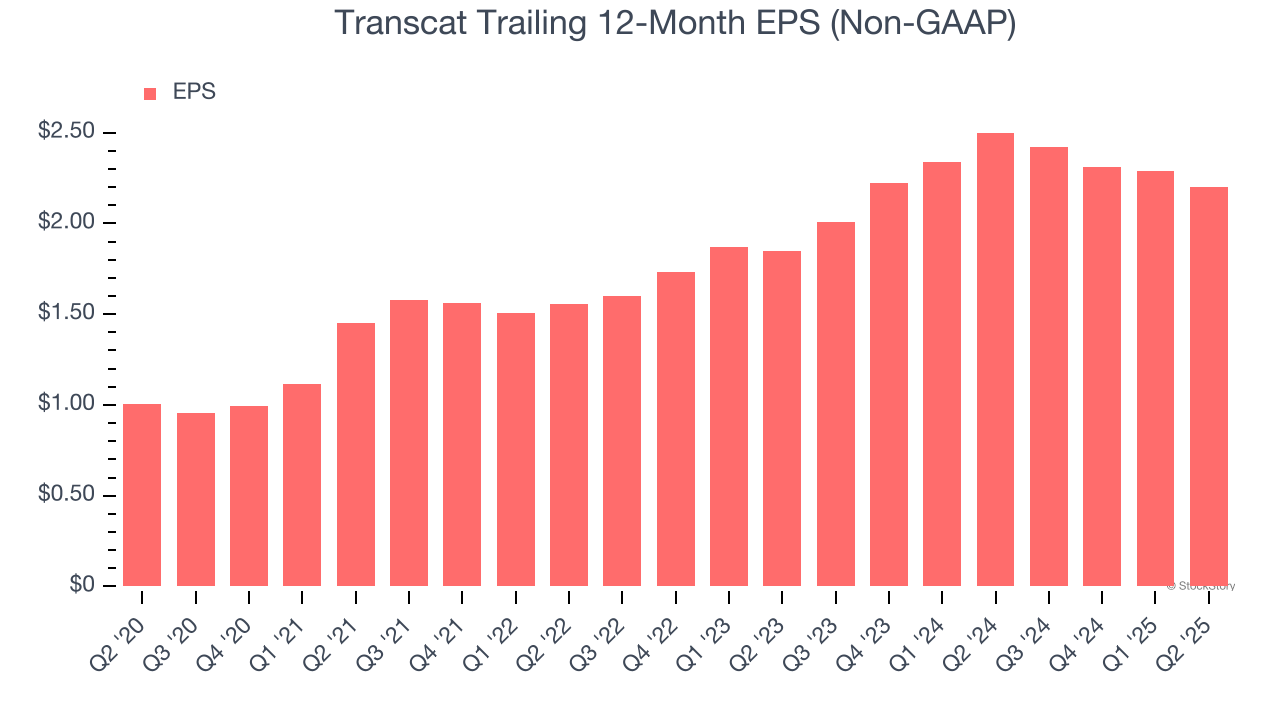

Transcat’s EPS grew at a spectacular 17% compounded annual growth rate over the last five years, higher than its 11.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Transcat, its two-year annual EPS growth of 9% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q2, Transcat reported adjusted EPS at $0.59, down from $0.68 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Transcat’s Q2 Results

We were impressed by how significantly Transcat blew past analysts’ revenue, EPS, and EBITDA expectations this quarter. Zooming out, we think this quarter featured some important positives. The stock remained flat at $77.92 immediately after reporting.

So should you invest in Transcat right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.